Is there really room for a brand-new TPA? Sidhartha Sinha thinks so — and he’s betting on AI to make it better than the rest.

As the CEO of Avant Health, he’s building an AI-native third-party administrator from the ground up to fix what he says are the industry’s most entrenched problems: outdated tech, poor member experiences, and missed opportunities to meaningfully lower costs. Goodbill sat down with Sid to hear what’s driving his vision — and why he believes care coordination, not claims systems, is the real unlock for better plans.

Interview edited for length and clarity.

Goodbill: Let's start at the beginning. What inspired you to make the leap from a data analytics vendor to standing up an entirely new TPA?

Sinha: We started in data analytics, and then we thought about going into decision support on the customer support and care coordination side. We started working with a couple TPAs. It was very tough. Response times getting access to data — it was just a terrible experience. Once, it took two months to get access to a dataset we’d requested.

Initially, I’d written off forming our own TPA, given all the compliance requirements and the product surface area. But after seeing how difficult it was to work with the incumbents, we took a step back. It’s a big undertaking, especially upfront. But we thought the longer-term outlook — whether commercially or just the impact we could have on members — was worth the tradeoff.

Goodbill: So being a point solution in this space, you didn’t feel like you could actually fix the things you wanted to fix?

Sinha: Yeah, point solutions are the secondary and tertiary decision makers in this world. Let’s say an employer is looking for fertility benefits, but they don’t have a good network. As a care navigation solution, I’d know that and can tell them that. But as a TPA, I not only know that — I can integrate and set it up for them, and solve their problem end-to-end.

"Point solutions are the secondary and tertiary decision makers in this world. But as a TPA, I can solve the [client's] problem end-to-end."

The traditional TPA model functions on legacy systems. One, you need a lot of people to operate these legacy systems. And two, there are data silos. TPAs have spent so much effort and resources trying to create unified systems, because the claim system doesn't talk to the customer support system, etc. What’s really cool in this world of AI agents is you no longer need a single unified data layer for most TPA services. We can set up agents and use cases and tasks, and tell it to get the data from wherever it sits. That’s a big differentiator, and how somebody with an AI-native model wins.

Goodbill: What's been harder than you expected in building a new TPA?

Sinha: Two things: The first is getting deals across the finish line — and in particular, deal qualification. You don’t always know which ones are going to actually close, under which timeline.

The second piece is financial reconciliation. There's so much variation on fixed costs, claims, percentage of savings. That’s been a large crash course, and I only still understand 70% of it.

Goodbill: Why do you think prospective clients are willing to give a brand-new TPA like yourself a shot?

Sinha: Part of it is desperation. One benefits advisor we’re working with has a saying: “All TPAs suck, and you just have to find that one that sucks the least.” Out of hundreds of conversations I've had with brokers, I can recall three or four where they said, “I like my TPA.”

"One benefits advisor we’re working with has a saying: 'All TPAs suck, and you just have to find that one that sucks the least.'"

The other side is that most people in the industry realize AI has benefits, but they don't fully know how to actualize them. So when we say we’re an “AI-native TPA,” it makes sense to them — in theory. The challenge is how we translate that for somebody to truly understand what that means. We’re educating as we’re selling.

Goodbill: So when you’re talking to a broker or employer who’s heard all the traditional pitches, how do you describe your differentiator in a way that lands?

Sinha: People have this canonical model of what a TPA is. The blocking and tackling, the claims adjudication, paying the claims — these are the No. 1 asks from brokers. So I first talk about the platform and how we make sure the claims come in, get audited, get paid on time.

But then where I spend a lot of time is actually on care coordination. What we've seen in the market — and nobody pushes back on this — is that care coordination reduces cost. If you're a self-insured employer, 70% of your budget is claims. The best way to reduce that cost is care coordination.

"What we've seen in the market — and nobody pushes back on this — is that care coordination reduces cost."

There are multiple layers to care coordination. Steerage is table stakes; but there’s also multimodal intervention, like: “Have you tried your Hinge Health benefit before you get that $90,000 knee surgery?” Another layer is disease management.

I describe that paradigm of care coordination, and how we’re leveraging the member experience — but also data other TPAs don't access. We’re getting more data, faster, so that we can intervene faster. That really resonates with people.

Goodbill: How do you explain the “AI” part?

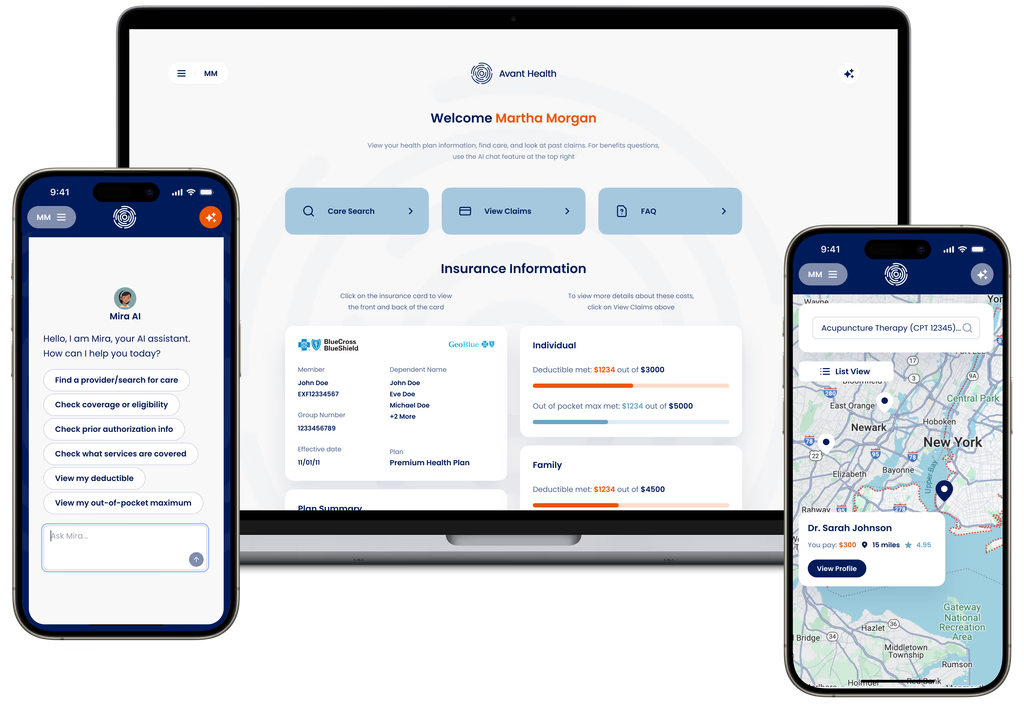

Sinha: Imagine you had one app on your phone that knew everything you wanted it to know related to your health: insurance, Apple Health information, your most recent lab visit, nutrition habits. We’re trying to create this “always-on” healthcare agent that engages and communicates based on their needs.

"We’re getting more data, faster, so that we can intervene faster. That really resonates with people."

We know that somebody on a high-deductible health plan is more likely to delay care until the end, and become more expensive than somebody on a PPO plan in the long run. So I should be engaging that person differently. Or, let’s say someone likes to engage with their insurance app at 7am, whereas someone else likes to do it at 11pm. I should use those archetypes to better engage people. Or, imagine somebody is on a diabetes care plan. It's been two months without an A1C blood test. I should reach out to the member and say, “Here are a couple of labs closest to you. Here are some available appointment times. Which one do you want to book?”

I need to serve that up on a platter for the member. Member experience is just a vector for care coordination. The thesis here is that people are not looking for optionality. We believe they want to be guided based on their specific needs and preferences.

"People are not looking for optionality. We believe they want to be guided based on their specific needs and preferences."

Goodbill: So how does the AI part look like in practice? How are you using AI, and what are the future opportunities with it?

Sinha: Think about the five or six TPA workflows around claims adjudication, care coordination, customer support, enrollment, compliance, analytics, and reporting. We asked ourselves where to — with limited resources — double down initially, because this is a phased approach.

We decided on customer support and care coordination, because we found it's a tangible pain point for HR managers, employers, and brokers. And when we demo what AI can do, and the ways it can help with member experience, it resonates a lot with them.

In practical application, it means we’re taking more data sets than a TPA is used to. Beyond claims, we're parsing other data sets, like raw encounter notes. The challenge becomes: How do you surface this up? Currently, we give members an experience that’s similar to what they're used to. I think the future is going to change — people will text, or they might have devices like AI glasses — but today, it's a simpler form factor. So the magic is really on the back-end: When do you choose to engage the member? What are you saying? What data are you leveraging?

Goodbill: What specifically are you asking AI to do for you?

Sinha: So let’s use an example on the customer support side. We found members tend to ask the same flavor of 7-10 questions: Am I covered for X? Do I need a prior authorization for Y? Can you help me find a cardiologist?

When somebody says they need help finding a cardiologist, we actually preemptively check eligibility. We check prior authorization requirements from the plan document. We then suggest providers that are in that area or meet preferences that we've stored for the member. Then we retrieve information and pricing about the provider. By the time we’ve answered this simple question, “Can you find me a cardiologist,” we've looked at three to five different data sets.

"By the time we’ve answered this simple question, “Can you find me a cardiologist,” we've looked at three to five different data sets. "

Prior to AI, imagine trying to unify all of those — it's just a mess, right? We use AI agents that each have a specific task but can go to these different data sets, and aggregate this information in a way that is presented cohesively to the member.

Goodbill: Who are the types of clients that are seeking you out right now?

Sinha: There are a couple of larger brokers that we’re partnering with that are more forward-thinking. The other place I'm seeing emerging signs of success is regional benefits advisors — those that are truly looking to customize health plans and not just offer an off-the-shelf cookie-cutter plan. We fit well because we can offer that level of flexibility.

On the employer side, the mid-sized groups are where you see the fastest adoption of self-funding. They have some amount of financial flexibility, or somebody willing to make decisions from the HR side, but they don't have enough leverage to get “big company” benefits. So we can help them bridge that gap.

A lot of groups we’re talking to are actually self-funding for the first time. Their benefits advisors have done a great job of educating them and saying, “If you go self-funded with a bigger TPA and network, you may get some improvement. But if you want a radical change, you're going to have to go with a very different kind of TPA.”

Goodbill: Where do you see your model headed over the next couple of years?

Sinha: I see ourselves as a TPA that plays a larger role in plan design, because we have the data. TPAs are so well-positioned to surface data for better plan design, but they haven't been able to do that for various reasons.

I believe the world is changing, and group health plans as we know them will cease to exist, or will exist in the minority. The world is going to transition towards more creative funding structures. We’re starting to see “self-insured plus ICHRA,” or “self-insured plus MEC” plans. There's a lot more variety because employers and people have different needs, so you're going to need hybrid models. That's where we're going to be best positioned to serve our clients.

"I believe the world is changing, and group health plans as we know them will cease to exist, or will exist in the minority."

Goodbill: Last question — if you could fast forward five years, what's one headline you'd love to read about your company?

Sinha: So much of this today is driven top-down from a broker or employer. Very rarely do you hear an employee say, “I want this insurance.” I would love to figure out a way that we can shift the paradigm.

So the headline would be: “Employees overwhelmingly want Avant Health as their insurance.” That, I think, shows we’ve gotten to the last person that we ultimately want to impact.

Interested in getting in touch with Sinha? Email him at sid@avanthealth.ai.

The latest news from Goodbill, including partnerships, product launches, and awards.

TPAs reveal where they want innovation, in Goodbill's poll of administrators across the country.

.jpg)

Employers are asking tougher questions, benefits advisors say.

Clearwater members now get access to Goodbill’s full suite of hospital savings services.